While the market for NAV financings—loans to funds supported by the net asset value of their portfolios—grew in 2023 and continues to rapidly evolve, a consensus has developed around what is sometimes referred to as a “Holdco Structure.”

The Holdco Structure is an approach used by a variety of borrowers and lenders across asset classes largely because it can address issues that repeatedly arise when negotiating and structuring NAV facilities. In Holdco Structures, the funds themselves are typically not borrowers. Instead, one or more holding companies directly or indirectly below the fund enter into the financing. Private equity NAV financings often go this route because they routinely use holding companies to address tax, regulatory, and other issues.

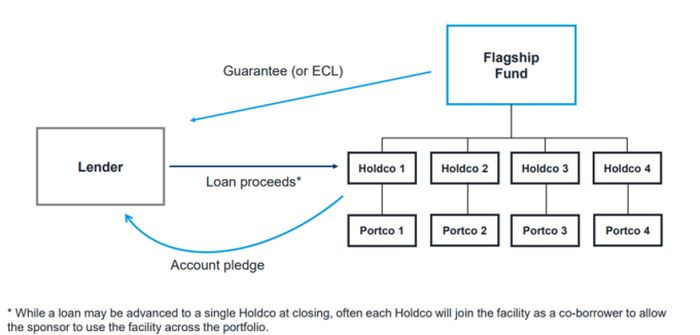

Of course, lenders typically require that each underlying asset that contributes to the portfolio NAV be owned, directly or indirectly, in whole or in part, by a borrower or guarantor. The Holdco Structure solves this issue through a co-borrower holding company obligor group, allowing for proceeds from a dividend, sale, or other liquidity event to be distributed up through the fund structure to the relevant holding company co-borrower. To the extent that there are one or more portfolio assets not owned by a co-borrower, those assets will be excluded from the NAV. Otherwise, the relevant holding company—or the fund itself—will be required to provide a guarantee or, in some cases, an equity commitment letter (see diagram below).

Holdco NAV Loan Structure

In the following article, we outline some important recurring issues that the Holdco Structure may address for parties considering entering into a NAV facility.

How Holdco Structures Work With Limited Partnership Agreements

A fund’s limited partnership agreement (LPA) typically will not expressly address the ability of the fund to enter into a NAV facility. Rather, the LPA’s debt restrictions often prevent the fund from directly incurring indebtedness other than in a few specific situations. For example, the LPA may allow for fund-level debt if the financing is short-term (i.e., it must be repaid within 60, 90, or 120 days). NAV financings, by contrast, typically provide for longer-term structural leverage, with maturities often ranging from three to five years. In other cases, some LPAs may allow for indebtedness solely to the extent that the financing represents only a certain portion of the capital commitments—20% to 30%, for example—or does not exceed the aggregate capital commitments altogether. NAV financings are sometimes put in place later in the lifecycle of a fund, by which point there may be little if any remaining uncalled capital.

The Holdco Structure, however, allows for a fund to enter into a NAV facility indirectly through one or more holding companies or other special-purpose vehicles. The LPA generally does not include applicable debt limitations at the portfolio level, as NAV financings are often entered into in the ordinary course with private equity, private credit, real estate, and various other strategies. Therefore, when a NAV facility is entered into at the holding-company level, the LPA restrictions may not apply to that indebtedness. Moreover, in many cases, the use of proceeds from a NAV facility may allow the borrower to refinance existing portfolio-level debt, finance follow-on investments, acquire additional portfolio assets, or engage in other portfolio-level activity that is generally consistent with customary financing activity of a leveraged strategy and permitted under an LPA. It is important to note, however, that throughout the structuring process, the sponsor will be in dialogue with its limited partners and other stakeholders about the potential use of a NAV facility.

Navigating Collateral Considerations

Most NAV financings do not include direct or indirect equity pledges of all portfolio assets, and in many cases, there is no equity pledged whatsoever. The collateral often will consist only of the accounts of the borrowers or guarantors and distributions of proceeds into those accounts. The primary reason for the lack of equity pledges is the restrictions found in portfolio-level loan documentation, including change-of-control provisions triggered upon a foreclosure, together with the broader pledge restrictions, often seen in preferred equity financings. In certain real estate NAV deals, even negative pledges may be problematic.

The Holdco Structure, however, still allows for full value capture for lenders, setting aside fraud or willful misconduct, because each holding company for each asset is usually required to be a co-borrower under the facility, or if not a co-borrower, then a guarantor. In this case, in the event of a sale in whole or part of a portfolio company or a dividend or other distribution off of the portfolio, the net proceeds must be distributed up to the holding company co-borrower or guarantor. Those proceeds will be held in a blocked account owned by that coborrower or guarantor with the release and application of the net proceeds for a standard cash sweep at the direction of the lender. In this case, again, other than as a result of a fraud, the net proceeds of a liquidity event would be subject to the lender’s control.

Guarantees and Using Equity Commitment Letters

Fund LPAs may limit the use of fund guarantees only to support debt repayment or other similar obligations of its portfolio companies. When that happens, particularly where the NAV facility proceeds are being deployed at the portfolio level (as opposed to being distributed to investors, for example), the fund may be able to provide a guarantee for the NAV facility. By contrast, in a NAV facility where the loan proceeds are being distributed in whole or part to investors, the Holdco Structure may allow, as an alternative, for a fund to provide an equity commitment letter (ECL) to one or more entities that are in the coborrower obligor group. Funds often have more contractual flexibility to capitalize holdings in their portfolios through additional equity infusions than to issue guarantees.

Targeted Financing or Refinancing for Specific Portfolio Company

The Holdco Structure also works well for sponsors that may need the loan proceeds for a specific portfolio company, such as to refinance a company’s existing debt. In this case, the Holdco Structure would allow for the relevant holding company or other indirect parent of the portfolio company to be the sole borrower.

The remaining portion of the NAV to support that refinancing could be conveyed through a fund-level

guarantee or ECL. In refinancing situations, it may also be possible to have the equity of that single portfolio company pledged to support the repayment of the NAV, together with the guarantee. With a single portfolio company, the sponsor may be able to obtain the needed consents within a reasonable period of time. While a financing for a specific portfolio company would appear on its face to potentially increase pricing, the Holdco Structure and the ability to have the full NAV of the fund support repayment of the financing avoids concentration risk and the associated higher pricing for more concentrated NAV financings.

Dealing With Existing Indebtedness

Sponsors often have various existing debt arrangements throughout the portfolio structure—including at the holding company level or elsewhere—that may be structurally subordinate to the location of the NAV financing. However, NAV financings, by definition, are intended to be subordinate to those lenders, and the placement of NAV debt at a holding company or other intermediate vehicle could adversely affect those lenders. To address these issues, the Holdco Structure allows for a significant amount of structural flexibility and may allow for the financing to be extended to one or more co-borrowers elsewhere in the fund’s organizational structure. For example, if indebtedness is in place at a holding-company level, the relevant co-borrower could be positioned to enter into the NAV facility on a subordinated basis directly at that level. Alternatively, the sponsor could consider having the NAV co-borrower placed directly above the holding company, subject to tax considerations, or have the parent entity of the holding company provide credit support through a guarantee or ECL.

Nuances for Tax-Exempt Investors

Tax-exempt limited partners such as certain pension plans and endowments are sensitive to unrelated business taxable income (UBTI). If the NAV facility were placed at the fund level or at a pass-through entity directly below the fund, these investors could potentially recognize debt-financed income, which is treated as UBTI for federal income tax purposes. In situations where a holding company co-borrower is treated as a corporation for U.S. tax purposes, the holding company may allow the fund to shield tax-exempt investors from UBTI.

Why the Holdco Structure Has Some Staying Power

While many aspects of the NAV financing markets continue to shift and evolve in response to sponsors’ financing needs and objectives, the Holdco Structure is being used with both large-cap sponsors—where most transactions are syndicated to banks and insurance companies—and middle-market and lower-middle-market sponsors, which are typically bilateral or club deals primarily financed by direct lending funds and other non-bank lenders. Many NAV transactions continue to be executed at the fund level or even portfolio company level, but we expect the market to continue to look to the Holdco Structure as a potential solution to a variety of recurring issues in the NAV space.